The Geopolitical Game of Thrones and Europe’s Energy Crisis

Ever since the Russia-Ukraine conflict started, it has evolved into an economic war between Russia, on the one side, and the European Union and the United States, on the other. While the US and the EU imposed heavy sanctions to cripple the Russian economy due to its actions in Ukraine, President Putin has played the geopolitical “Game of Thrones” so well that now Europe is facing an economic crisis. The EU annual inflation rate for energy has touched a record high of 42%, food inflation has increased to 9.8% – the highest in 20 years –, and now the GDP growth rate is slowing down, with Russia being blamed for this. At the same time, rising inflation is ending an era of negative real interest rates and increasing the risk of a fracturing Eurozone economy.

Euro Area annual inflation and its main components, July 2012- July 2022 (%)

Source: Eurostat.

Meanwhile, the worst is yet to come to Europe because “winter is coming”!

Now the obvious questions are:

- How did Europe end up in such a terrible state?

- How come the European leaders are unable to decode Putin’s war strategy to choke Europe?

To get an answer to these two questions, we need to first understand the basics of modern warfare and its grounding in economic warfare. This study intends to analyze the energy crisis challenges, the weaponization of economic policies, and their implications for European businesses and households.

The current geopolitical war is being fought on three fronts - food, finance, and energy. The EU measures prohibit the export of dual-use goods as well as those goods that can contribute to Russia’s defense and security capabilities, including industrial producers’ goods; prohibit public financing or financial assistance for trade with/or investment in Russia; prohibit the export of goods and technology for use in oil refining and impose a set of prohibitions in the aviation sector. In addition, the measures ban a range of financial interactions and transactions with Russia.

- On 28 February 2022, the European Council adopted further measures, which include the prohibition on all transactions with the Central Bank of the Russian Federation and a prohibition on the overflight of EU airspace and access to EU airports by Russian carriers.

- On 1 March 2022, the Council introduced further measures excluding key Russian banks from the SWIFT system.

- On 9 March 2022, the Council adopted further measures concerning the export of maritime navigation goods and radio communication technology to Russia.

- On 15 March 2022, the Council introduced another package of sectoral economic measures. These measures include further financial and trade prohibitions.

- From 16 April 2022, EU sanctions prohibit vessels registered under the flag of Russia from accessing EU ports(European Commission, 2022). This also applies to vessels that have re-registered from the flag of Russia to the flag of another state after 24 February 2022 (Department of Enterprise, Trade and Employment, 2022).

All these EU sanctions coupled with those of the US were expected to drive the Russian economy into bankruptcy. Even though the EU can argue that they are winning on the finance front, the story is different on the food front since Russia and Ukraine accounted for about 30% of global wheat exports, 20% of corn exports, and 80% of sunflower oil supply. The military blockade on the Black Sea led to supply constraints of these food commodities, hence food inflation in Europe and across the globe.

Russia & Ukraine Global Food Export %

Source: Comtrade.

As far as Russia is concerned, the energy front is where it has the most leverage against Europe. As of January 2022, 45% of Europe’s gas came from Russia. The main source of the gas supply from Russia is the Nord Stream 1 pipeline. This pipeline delivers 55 billion cubic meters of gas per year (104,642 cubic meters per minute) or nearly 40% of Europe’s total pipeline imports from Russia through the Baltic Sea.

Europe and its friend, the US, have made public statements on how they can do without Russian gas, but the reality is that they cannot, at least not in the short or medium term. On March 25, President Joe Biden pitched himself as the EU's savior from its Russian energy addiction. After five months, the US was still unable to meet its commitment. Part of President Biden’s agenda for visiting Saudi Arabia in July was to convince Mohammed bin Salman Al Saud, the Crown Prince of Saudi Arabia, to boost OPEC oil production to cover Russia’s supply and stop rising energy prices. However, the Crown Prince was not willing to do so, since a low supply of oil will automatically lead to higher prices in favor of Saudi Arabia – the 2nd largest oil producer in the world, and an ally of Russia in the OPEC-Plus in regulating the market for oil supply and price management. Note that, according to current estimates, 80.4% (1,241.82 billion barrels) of the world's proven oil reserves are in OPEC Member Countries, with the bulk of OPEC oil reserves in the Middle East, amounting to 67.1%, and Saudi Arabia accounting for 21.5% of the OPEC total (OPEC, 2022). If Saudi Arabia is getting a super high price for its oil and gas, what then would be the incentive to want to force the price down by increasing the market supply when Saudi Arabia can make extra revenue due to the market shortage? Therefore, despite sanctions, pressure, and propaganda, Europe is still at the mercy of Russia for the winter.

As Europe continues in its struggle to put out fires hurting its economy on several fronts, the rising cost of heating homes and feeding families becomes the most worrisome factor in many Europeans’ minds. At 95% YoY increase, the price of heating gas oil (red diesel) has outpaced the speed of increase of other fuel products, which grew by 40% YoY on average. The importance of heating homes has thus made the bloc agree on a plan to cut gas consumption by 15% by March 2023 as Moscow announced another cut to supply.

Crude oil price trend

Source: Trading Economics.

Consumer prices of petroleum products inclusive of duties and taxes - EU27_2020 weighted average

Source: Trading Economics.

Since Russia forces the “unfriendly” states to pay for their gas imports in rubles, the exchange rate of the Russian currency has shot up; hence, making the ruble the best-performing currency in the world. In July 2022, the Russian ruble hit its strongest level in 7 years despite sanctions. Over the last 12 months, its price rose by 24.14%. The exchange rate of the ruble was at 60 per USD in August, remaining well above levels before Russia invaded Ukraine and cementing its rebound from the record low of 150 touched in March, supported by strict capital controls and trade imbalances. Looking ahead, the Ruble to USD rate is expected to be priced at 64.83 by the end of Q3 2022 and at 82.81 in a year according to global macro models projections and industry analysts’ expectations. (Trading Economics, 2022)

Ruble to US Dollar exchange rate trend

Source: Trading Economics.

As far as Europe is concerned, the increasing energy prices have a ripple effect on industrial production costs, leading to higher inflation. For Russia, higher prices for energy and commodities since the start of the war lifted export revenues and relative ruble demand amid a collapse in importing activity due to sanctions. On top of that, the Central Bank promoted a loose monetary policy and cut interest rates. The disparity is reflected in the widest current account surplus on record of USD 70.1 billion in Q2 2022 from USD 17.3 billion in the corresponding period of the previous year — this is a 305% YoY increase. Strength in the ruble persisted even as the Central Bank of the Russian Federation cut borrowing costs to below pre-invasion levels, amid continuous weekly deflation readings.

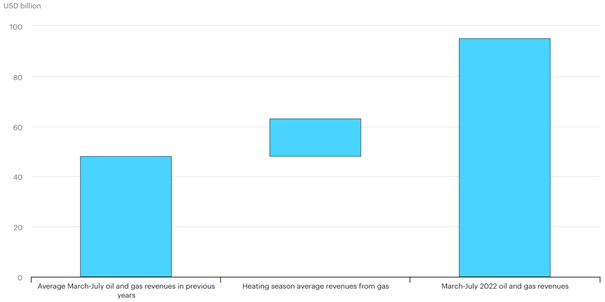

Despite selling less oil and gas to Europe during the Ukraine invasion, Russia was able to generate more revenue from these commodity exports during the invasion than before the invasion of Ukraine, even with all of the sanctions in place. Looking at Russia’s revenue from oil and gas exported to Europe, the average is about USD 50 billion from March – July, but this revenue has almost doubled in 2022. Russia’s oil and gas export revenue in the last 5 months has tripled what it would typically earn from Europe during the winter season.

Russia's oil and gas export revenues from the European Union

Source: IEA.

Russia is Europe’s largest supplier of natural gas, oil, and coal, and has become ingrained in distribution networks. What is surprising is that the energy crisis in Europe has been building for a while, and Russia’s role in it has been clear from the beginning. After Russia invaded Ukraine on 24 February 2022 and Europe took the side of Ukraine, nobody in Europe or elsewhere should have been under any illusion about the risks surrounding the Russian energy supplies.

Russian Pipeline gas supplies to EU by Route (Million Cubic Meter)

Source: ENTS.

Following recent cuts in deliveries, mainly through the Nord Stream 1 pipeline, Russian pipeline exports to the EU are now down roughly 60% compared to June 2021, for what Russia says is planned maintenance. It remains unclear whether the pipeline will resume and, if so, at what level. Additional risks to supply could come via potential wartime destruction of energy transmission infrastructure, further sanctions on Russian energy exports by European policymakers, or embargoes on exports by Russia. To date, disruptions to the gas, oil, and coal trade—and concerns over future supply—have led to large spikes in energy prices.

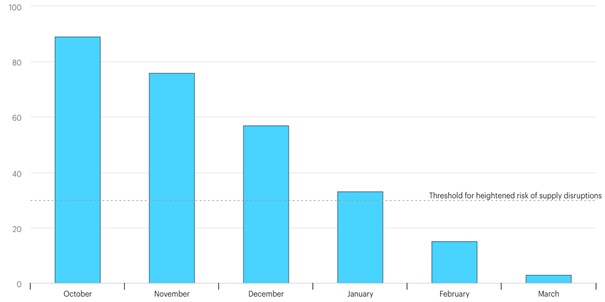

According to (IEA, 2022) projection, even with gas storage at 90%, the EU would face a heightened risk of supply disruptions if there were a complete Russian cut-off. The withdrawal ability of storage sites is significantly reduced when inventory levels fall below 30% of working storage capacity, due to the drop in reservoir pressure.

Potential evolution of EU Gas storage levels in event of a complete Russian supply cut, from October 2022

Source: IEA.

With Europe's geographical proximity to Russia, the continent cannot ignore the importance of the Russian Federation because natural gas is crucial to its energy security and economic stability. Russia happens to have the largest natural gas reserves in the world to the tune of 38 trillion cubic meters. While there is sufficient pipeline infrastructure to ensure the seamless transportation of natural gas from Russia to Europe, the same cannot be said for the US or other countries of the world for the shipping infrastructure that is required to import gas into Europe. The US is clearly not a viable alternative to Russia at least not in the short or midterm. The US can only provide Europe with Liquefied Natural Gas, which is more expensive to be shipped across the Atlantic. Unfortunately, LNG cannot fill the gap that the absence of Russian gas will create for Europe. Establishing shipping infrastructure with the US for the transport of gas will take years, and Europe is running out of time.

So, Europe’s biggest challenge is that it is categorically not enough to just rely on gas from other sources but Russia because natural gas is not fungible and is dependent not only on production but also on infrastructure that is very difficult to re-orient. These supplies are simply not available in the volumes required to substitute for missing deliveries from Russia. This will be the case even if gas supplies from Norway and Azerbaijan flow at maximum capacity, if deliveries from North Africa stay close to last year’s levels, if domestic gas production in Europe continues to follow recent trends, and if inflows of LNG increase at a similar record rate as they did in the first half of this year. That is already a lot of “ifs”.

As stated earlier, the worst is yet to come to Europe because “winter is coming” and President Putin is just playing the waiting game. This winter would become a historic test of European solidarity – one it cannot afford to fail – with implications far beyond the energy sector.

References

Department of Enterprise, Trade and Employment. (2022, July 20). EU trade sanctions in response to situation in Ukraine. Retrieved from Enterprise Information Centre: https://www.enterprise.gov.ie/en/publications/eu-trade-sanctions-in-response-to-situation-in-ukraine-.html#:~:text=breaching%20the%20sanctions.-,Importation%20of%20goods%20using%20Russian%2Dflagged%20vessels,state%20after%2024%20February%202022.

European Commission. (2022, July 25). EU Sanctions Map. Retrieved from Sanctions Map: https://www.sanctionsmap.eu/#/main/details/26/?search=%7B%22value%22:%22%22,%22searchType%22:%7B%7D%7D.

Eurostat. (2022, July 29). Euro area annual inflation rate and its main components. Retrieved from ec.europa.eu/: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Inflation_in_the_euro_area.

IEA. (2022, July 18). Even with gas storage at 90%, the European Union would face heightened risk of supply disruptions if there is a complete Russian cut-off. Paris: IEA. Retrieved August 6, 2022, from IEA: https://www.iea.org/data-and-statistics/charts/even-with-gas-storage-at-90-the-european-union-would-face-heightened-risk-of-supply-disruptions-if-there-is-a-complete-russian-cut-off.

IEA. (2022). Russian natural gas flow to the European Union, January 2019-July 2022. Paris: IEA. Retrieved August 6, 2022, from https://www.iea.org/data-and-statistics/charts/russian-natural-gas-flow-to-the-european-union-january-2019-july-2022.

IEA. (2022, July). Russia's oil and gas export revenues from the European Union. Paris: IEA. Retrieved August 6, 2022, from IEA: https://www.iea.org/data-and-statistics/charts/russia-s-oil-and-gas-export-revenues-from-the-european-union.

OPEC. (2022). OPEC Annual Statistical Bulletin. OPEC. Retrieved from https://www.opec.org/opec_web/en/data_graphs/330.htm.

Trading Economics. (2022, August 4). RUBUSD Russian Ruble US Dollar. Retrieved August 5, 2022, from Trading Economics: https://tradingeconomics.com/rubusd:cur.